End of Tax Year Planning 2021

Well, it has been quite a year since our last End of Tax year email, hasn’t it! To reassure you, this note has nothing to do with homeschooling, social distancing, masks, not getting an Ocado order for 6 weeks because people are panic buying toilet roll or planning where to go on your 6775th walk of the week. Instead, this is a nice, straightforward ‘to do’ list of actions that you should take before the 6th April.

Please do get in touch if you want to tick any of these off before the end of tax year deadline.

PENSIONS

Personal contributions to a pension offer tax relief at your highest rate (maximum of 45%), subject to an annual contribution limit. In addition, you can look back 3 tax years to mop up any unused relief. The 17/18 tax year will fall away after the 6th April, so it’s a use it or lose it opportunity. We don’t know what Rishi has up his sleeve and so if you can contribute, you should.

You can contribute up to £40,000 per year and still receive tax relief at your highest rate, however, the amount you can contribute is restricted for anyone earning over £240,000 and it could be as low as £4,000 per year. You can still take advantage of unused contributions from previous years, dating back 3 tax years to really give your retirement planning a boost.

There are continued whispers that the tax relief system is going to change – a flat rate of 25% is what is being considered and so you should take advantage now if you can.

Did you know?

The taper relief rules for high earners has changed and this may mean you have more capacity than you thought to make a pension contribution.

INDIVIDUAL SAVINGS ACCOUNTS (ISA)

There is no income tax or capital gains tax payable on ISA proceeds, making them the most tax-efficient savings vehicle in the medium to long-term. The maximum contribution you can make is £20,000 per person, per year. You cannot carry over your ISA allowance and once the year has ended, it is lost.

Did you know?

Even though the rules changed a while ago, not many people know that you can remove funds from an ISA and put them back again, provided the ISA is classed as ‘flexible’ and the transaction is done in the same tax year. So if you have made any withdrawals this tax year, there is still room to put them back.

JUNIOR ISA

For those of you with children (and grandchildren) who do not have an existing Child Trust Fund (you aren’t allowed a Junior ISA if you have a Child Trust Fund), a Junior ISA is a tax efficient way to build up funds for the future. They work in the same way as your own ISA; however, the maximum investment is £9,000 per child.

CAPITAL GAINS TAX

Every individual is entitled to a Capital Gains Tax (CGT) annual exemption and this is currently £12,300. CGT rates are 10% for a basic rate taxpayer and 20% for the higher rate. It is 18% and 28% respectively on residential property. The recent budget froze the annual exempt allowance and rates of tax until 2026.

Did you know?

Each person has the tax-free allowance. If you pay the higher rates of tax and hold shares which are providing a taxable income and your spouse is either a non- or a basic rate taxpayer, you could look to transfer the shares into their name. There would be no immediate CGT implications and your taxable income is reduced.

Capital losses can also be used to offset gains and if appropriate for you, this is something we can look at before the end of the tax year.

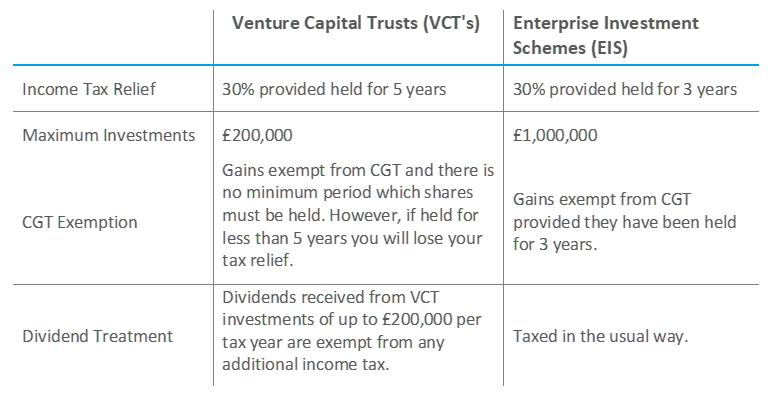

VENTURE CAPITAL TRUSTS (VCT) & ENTERPRISE INVESTMENT SCHEMES (EIS)

As well as the simpler tax planning ideas there are other higher risk and more complex areas, such as Venture Capital Trusts and Enterprise Investment Schemes, which are tax year end sensitive. These are traditionally higher risk investments but can offer up to 30% tax relief and provide diversification of your portfolio. In addition, the underlying investments offer interesting investment opportunities which you may not otherwise be able to access.

The table below shows the main tax advantages.

GIFTING FOR INHERITANCE TAX PURPOSES

You can give away gifts worth up to £3,000 in each tax year and these gifts will be exempt from Inheritance Tax when you die. You can of course gift more than this at any time in the year, and if you survive 7 years from the date of the gift, that too will be outside of your estate.

Certain gifts don’t use up this annual exemption, however, there is still no Inheritance Tax due on them. For example, wedding gifts of up to £5,000 for a child, £2,500 for a grandchild (or great-grandchild) and £1,000 to anyone else. Individual gifts worth up to £250 are also free of Inheritance Tax.

Did you know?

You can carry forward any unused part of the £3,000 exemption to the following year, but if you don’t use it in that year, the carried-over exemption expires.

If you would like to get ahead of the game and take advantage of these end of tax year planning suggestions, please get in touch now.

The information in this blog is for your general information and use and is not intended to address your particular requirements. Specifically, the information does not constitute any form of advice or recommendation by Carrington Wealth Management and is not intended to be relied upon by users in making (or refraining from making) any investment decisions. It is important to remember that the value of your investments can go down as well as up, and you may not get back the amount you invested. Past performance is not necessarily a guide to future performance. Please contact us for appropriate independent advice, which should be obtained before making any such decisions.

")