Q2 2023 Investment Commentary & Webinar

Welcome to our latest investment commentary covering the second quarter of 2023. We hope you and your family are well and that you are looking forward to the summer holidays.

Before jumping into the meat of the commentary, we have included a recording of our recent investment webinar, which took place on Monday, 10th July.

If you were unable to join Tommy and me on Monday or you would like to revisit what we discussed, please click on the image below.

Our webinars are produced for information purposes only and do not constitute financial advice.

With the volatility seen at the end of Q1, following the collapse of Silicon Valley Bank and Credit Suisse, the markets were somewhat quieter during Q2 and we are pleased to report that most of the portfolios ended with small positive gains.

Whilst general conditions remain difficult, with ever increasing interest rates, it has been our ongoing stance to remain invested throughout this period.

Our base case is that economic conditions will remain challenged into the end of this year and next year, as higher interest rates slowly work their way through the system. For this reason, we have focussed on thinking of ways to insulate the portfolios from unintended market events. However, economic conditions may turn out to be better than expected and we do not know when the next economic cycle could begin. Therefore, we have worked hard at creating a blend in portfolios that can capture positive market movements whilst protecting from any unexpected negative outcomes.

Q2 REFLECTIONS

Much of the quarter was dominated by two themes; the talk of higher interest rates and excitement around the prospects of Artificial Intelligence. Both of these topics were covered in our webinar – link above.

Before we cover those themes, it’s worth noting the strength of the Pound against the US Dollar. Since the mini-budget at the end of September last year, the Pound has been steadily appreciating against the US Dollar. This has reduced the gains achieved from our US holdings which are denominated in US Dollars. Q2 2023 was no different, with the Pound moving higher and leading to an approximately 10% impact on the returns from our US holdings for 2023 so far.

The US Federal Reserve finally paused its interest rate hikes after nine consecutive increases. However, they noted that they envisage hiking them again later this year, with potentially two more hikes to come. Initially sceptical of their plans, the markets have started to buy into the narrative due to more positive economic data being seen, suggesting the Fed has reasons to continue hiking. The European Central Bank and Bank of England have echoed the Fed, indicating that the developed world has not yet seen the end of the current hiking cycle.

Whilst there was no song and dance about it, the US Fed had resumed a degree of Quantitative Easing (QE) following the collapse of Silicon Valley Bank. Several regional US banks linked to the start-up Tech scene and US commercial property were running into trouble due to the higher interest rate environment. To prevent a systemic crisis, the Fed stepped in to provide liquidity to these banks, as well as others. This of course is at odds with the general messaging from the Fed, where they have been keen to withdraw liquidity.

Lastly, the emergence of Chat GPT4 (AI software) at the end of Q1, led to a frenzy in certain associated markets/companies, with the likes of Nvidia seeing a 200% increase in their share price. Chat GPT and other AI tools have demonstrated remarkable abilities since Q4 of last year. There is genuine concern around the viability of certain professions both in the short and long term, with the potential for many parts of the corporate world seeing productivity improvements.

One further point worth noting is the strength of the Pound against the US Dollar. Since the mini-budget at the end of September last year, the Pound has been steadily appreciating against the US Dollar. This has reduced the gains achieved from our US holdings which are denominated in US Dollars. Q2 2023 was no different, with the Pound strengthening further leading to an approximately 10% impact on the returns from our US holdings.

We made a few small changes over the quarter, with the focus being on building our protective strategies and adjusting position sizes away from the more economically sensitive parts of the portfolios. The more significant changes were done last year and they are continuing to work at present. We are pleased with the current positioning in the portfolios and continue to look for opportunities that develop as a result of the market conditions.

Q2 REVIEW

Market Performance

Year on year US CPI (inflation) continued to fall over the quarter, coming down to 4.0%. It was again encouraging to see the core components also easing back in the recent data releases, which are more of a focus for the US Fed. Once again, UK CPI has remained stubbornly high at 8.7%, which means the UK is increasingly becoming an outlier amongst developed nations.

Broadly speaking, equities and bonds moved in tandem over the quarter, with most equity and bond markets delivering flat to negative returns. However, due to the short-term QE from the US Fed and hype around AI, US equity markets performed well. We have previously talked about our overall strategy and that our largest Geographical exposure remains to the US in portfolios, helping many to eke out a positive gain.

Whilst not offering anything noteworthy this quarter, Government bonds continue to be a key focus for us. We have continued to add to our Government bond positions which we believe could add a lot of value when the current interest rate hikes are finally behind us.

We continued to see sector dispersions, with Technology comfortably being the best performer due to the AI frenzy. In contrast with the 2022 theme, the Consumer Discretionary and Technology sectors have continued to be the best performers this year. The repeated swings between the different groups of sectors is something we have been seeking to avoid and which backs up our stance to be generally sector neutral, with a slight overweight to the Defensive sectors such as Healthcare and Consumer Staples. This approach has led to a drop in our volatility levels and good relative performance.

2023 OUTLOOK

Inflation & Central Banks

In aggregate, inflation in the Developed world continues to fall but the inflation picture is Geographically dependent. Each region increasingly has its own idiosyncratic reasons behind its respective inflation stories. For China, the word ‘deflation’ has returned, with CPI falling to 0.2% over the past year.

Energy and broader commodity prices have remained subdued, helping to reduce the year-on-year inflation data for those most sensitive to these prices such as Europe. Furthermore, the core components of inflation are also showing signs of easing back in several regions. This is of course a positive sign.

The various Central Banks have talked up the prospect of higher interest rates again. The reason for this, despite inflation falling, is that the monetary policy so far has not had the desired effect on the labour markets. In the US, the labour markets remain robust and unemployment low. For inflation to well and truly abate, the Fed need to see some deterioration in the labour markets. Due to the uncertainty here, the environment could remain volatile and certain industries could come under pressure as conditions continue to tighten.

We expect inflationary pressures to continue easing over the coming months but to settle above the medium-term historical average of 2%. We would not be surprised if inflation remained above 4% over the coming years and averaged a higher figure.

Recession Risk

We have spoken at length about our views on recession risks in previous commentaries. Nothing much has changed since, with some economic data (especially manufacturing) being poor but labour market data being good.

We are continuing to see signs of recessionary risks, with indicators across a range of segments deteriorating. This should not come as a surprise due to the aggressive monetary policy we have seen.

Recessions do not always spell bad news for the markets because it depends on the type of recession experienced. We have positioned the portfolios defensively as mentioned earlier and do not expect to increase the risk levels until the outlook improves.

As previously mentioned, Government bonds can perform well in such an environment which explains our focus on this market. They are seen as safe haven assets during such times and we have been steadily increasing our exposure to them. They are particularly effective when Central Banks begin cutting interest rates.

Strategy

As mentioned at the start of the update, we have remained fully invested but have adjusted the positioning to reduce the volatility levels and better navigate the current environment. Some points to note around our thinking moving forwards, which generally follow the comments in our previous updates:

- We continue to believe elevated volatility levels are likely to become a feature of markets over the next few years and so we will maintain a lower volatility approach more frequently.

- We have already leaned into a range of bonds with a greater focus on Government bonds, which can act as an effective hedge against equity market volatility. We have now completed this process.

- Outside of Government Bonds, we have concentrated our exposure in short-dated investment grade bonds, which are the safest corporate bonds to invest in. The yields remain attractive.

- In terms of our equity allocations, our largest equity exposure remains towards US markets however, we are maintaining good allocations to other markets such as Asia. Diversification is key in this environment.

- As previously mentioned, we now have no direct exposure to Europe due to the ongoing war in Ukraine. On a look through basis, some of our global funds have select European exposures and these are typically in the high-quality international companies such as Roche and ASML.

- We are not changing the allocation to the UK and have maintained a focus on the large, international FTSE businesses. We remain concerned with the domestic outlook and feel there are risks that may not be obvious. We are therefore avoiding small and mid-sized businesses, however, we do believe an opportunity will come along eventually to add to smaller companies and so we have done a lot of research work in this area.

- We continue to hold a reasonable amount of Asian equities and are thinking to expand into other Emerging Markets. Valuations are very compelling and they generally do not face the same inflation/interest rate policy headwinds.

You should note that when we see signs of improvement and the potential for interest rates to fall, we are likely to increase our risk levels and focus on areas that typically do well during the recovery periods such as Financials, Industrials and Materials businesses.

Summary

Whilst the markets have been drifting higher since October 2022, we are monitoring the fast-changing developments and the prospect for recessionary risks to take centre stage. We have been adjusting the portfolios accordingly.

We will continue to look for new opportunities for the portfolios whilst trying to navigate the environment the best we can.

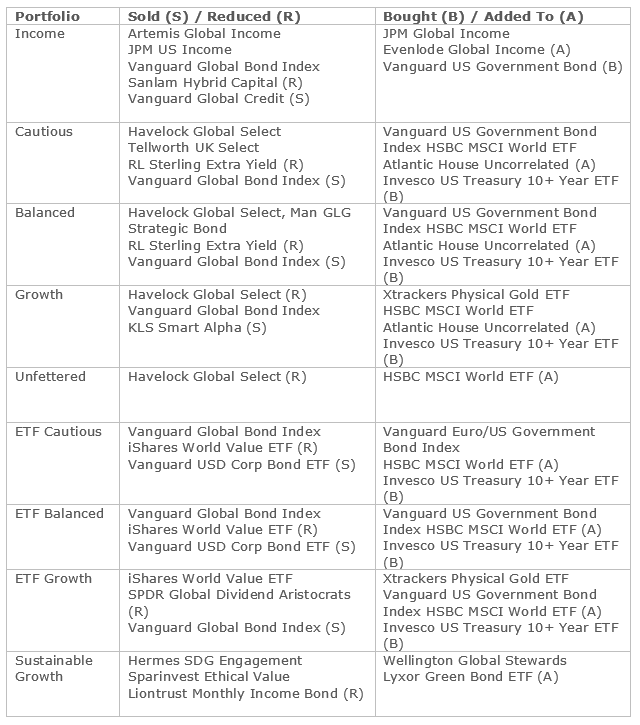

CHANGES MADE

Below is a table summarising the changes made over the quarter in the portfolios.

We hope you find this review informative and look forward to hearing from you if you have any questions.

IMPORTANT: This publication has been prepared for information purposes only by Carrington Investment Consultants Ltd. The value of investments, and any income generated from them, will be affected by interest rates, exchange rates, general market conditions and other political, social and economic developments, as well as by specific matters relating to the assets in which it invests. Investors should be aware that the value of units may well fall as well as rise, is not guaranteed and that past performance is not a guide to future performance. Different funds carry different levels of risk and investors may not get back the full amount invested. Carrington Wealth Management is a trading style of Carrington Investment Consultants Limited which is authorised and regulated by the Financial Conduct Authority. Registered office: One Chapel Place, London W1G 0BG. Registered in England, number 3193939. This email and any accompanying documents contain confidential information intended for a specific individual which is private and protected by law. If you are not the intended recipient, any disclosure, copying, distribution or other use of this information is strictly prohibited. You are also requested to advise us immediately if you receive information which is not addressed to you. Data Source: Financial Express. Copyright © Carrington Wealth Management. All rights reserved.