Spring into Action with End of Tax Year Planning

It’s worth noting that the Spring Budget is planned for the 23rd March this year – the Autumn statement was cancelled so we may see some changes announced in the Budget that may well impact your future financial planning. So, as usual, we wanted to remind you of all the main planning points you should consider before the end of the Tax Year – or more realistically, before the 23rd March.

- Pay the maximum you can afford into your pension

- Carry forward unused pension contributions

- Pay into your spouse’s pension

- Use your ISA Allowance (LISAs should also be considered)

- Pay into your child or grandchild’s JISA or pension (max £3,600 per year)

- Consider VCT or EIS investments

- Gifting to reduce your estate for Inheritance Tax purposes

PENSIONS

You can contribute up to £40,000 per year and still receive tax relief at your highest rate, however, the amount you can contribute is restricted for anyone earning over £240,000, and it could be as low as £4,000 per year. You can still take advantage of unused contributions from previous years, dating back 3 tax years to really give your retirement planning a boost.

There are continued whispers that pension funding will be changed in some way – removing the carry forward facility seems like an easy win for the Government, so let us look at this while it’s still available to you.

INDIVIDUAL SAVINGS ACCOUNTS (ISA)

There is no income tax or capital gains tax payable on ISA proceeds, making them the most tax efficient savings vehicle in the medium to long term. The annual ISA contribution limit is £20,000 per person per annum. You cannot carry over your ISA allowance and once the year has ended, it is lost. However, if you have taken money out of an ISA this year, you have until 5th April to put it back.

JUNIOR ISA

For those of you with children (and grandchildren) who do not have an existing Child Trust Fund (you aren’t allowed a Junior ISA if you have a Child Trust Fund), a Junior ISA is a tax efficient way to build up funds for the future. They work in the same way as your own ISA; however, the maximum investment is £9,000 per child per year.

LIFETIME ISA (LISA)

Provided you are over 18 and under 40, you are able to use a LISA to help buy your first home, or to fund retirement. You can fund up to £4,000 per year (this forms part of the overall £20,000 ISA allowance) until you are 50, and the Government will add a bonus of 25% per year – up to £1,000 per year. *There are certain criteria to using these investment vehicles, please contact us to find out if they are appropriate for your needs.

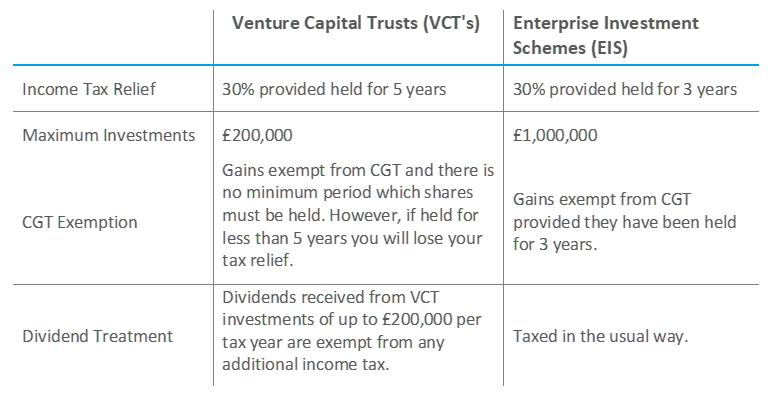

VENTURE CAPITAL TRUSTS (VCT) & ENTERPRISE INVESTMENT SCHEMES (EIS)

Whilst VCTs and EIS investments are not for everyone, they are a useful tax-efficient investment to consider once you have funded your ISAs and pension.

These are traditionally higher-risk investments but can offer up to 30% tax relief and provide diversification of your portfolio. In addition, the underlying investments offer interesting investment opportunities which you may not otherwise be able to access.

The table below shows the main tax advantages.

GIFTING FOR INHERITANCE TAX PURPOSES

You can give away gifts worth up to £3,000 in each tax year and these gifts will be exempt from Inheritance Tax when you die. You can of course gift more than this at any time in the year, and if you survive 7 years from the date of the gift, that too will be outside of your estate. Certain gifts don’t use up this annual exemption, however, there is still no Inheritance Tax due on them. For example, wedding gifts of up to £5,000 for a child, £2,500 for a grandchild (or great-grandchild) and £1,000 to anyone else. Individual gifts worth up to £250 are also free of Inheritance Tax.

If you would like to take advantage of any of these end of tax year planning suggestions prior to the budget announcement, please be in touch soonest so that we can advise you further.

This publication has been prepared for information purposes only by Carrington Investment Consultants Ltd t/a Carrington Wealth Management and does not constitute financial advice. The value of investments, and any income generated from them, will be affected by interest rates, exchange rates, general market conditions and other political, social and economic developments, as well as by specific matters relating to the assets in which it invests. Investors should be aware that the value of units may well fall as well as rise, is not guaranteed and that past performance is not a guide to future performance. Different funds carry different levels of risk and investors may not get back the full amount invested.