Q4 MARKET UPDATE & MARKET INSIGHTS WEBINAR

Happy New Year. We hope you have a prosperous and healthy year ahead.

Welcome to our latest investment commentary covering the final quarter, and 2022 as a whole. Before we begin, we wanted to share some broader thoughts with you.

2022 turned out to be a rare event in investment terms, with both equities and bonds falling by similar magnitudes. We have only seen such an outcome a handful of times over the past century. As we have mentioned previously, other asset classes such as Gold also struggled, making it an exceptionally difficult environment in which to manage both low and high risk diversified portfolios. 2022 follows a few volatile years for markets, particularly in 2020.

We continue to emphasise that this period of weakness won’t last forever, and although this may be unsettling, we encourage you to focus on your long term goals.

On a positive note, in our previous market commentary, we mentioned three potential catalysts that could help give the markets a lift. We are pleased to report that two of the three events (summarised below) are starting to have an effect.

- The end of the Ukraine war

- The US Federal Reserve slowing the pace of interest rate hikes

- China developing a Covid vaccine and ending their restrictive Covid policy

Firstly, the US Federal Reserve has now indicated a slow down, and then pause, in the interest rate hiking cycle this year, helping to give the markets some support. This catalyst has plenty of runway yet but is now in progress.

Although a Covid vaccine is yet to materialise, public discontent pressurised the Chinese Government, forcing them to dramatically reduce the Covid restrictions in place. This has had a positive effect, especially for Asian markets.

It is unfortunate to see the war has continued in Ukraine and the Unfortunately, the war has continued in Ukraine and the indications are currently for a protracted conflict. Our thoughts remain with the people of Ukraine and the millions displaced by the war.

More detail on the above can be found later in the note.

It has been our ongoing stance to remain invested throughout this period because we did not know when these, and other less obvious catalysts could come to fruition. We have instead worked hard at helping the portfolios navigate the current environment, with several changes being made over the past year.

Q4 REFLECTIONS

Following the end of Q3 weakness, October and November were positive months in the markets and the portfolios spent much of the time recovering from their low points. Sadly, the seasonal Santa rally failed to arrive and December was a generally flat month. The overall quarter however was positive.

Once again, a similar set of factors were in play with higher interest rates, the war in Ukraine and recession concerns adding to the mix. Early in the quarter, China’s zero Covid policy also gained some air time, compounding the global concerns.

However, there were some bright spots, particularly in the latter half of the quarter. As we had expected, data from November onwards confirmed easing inflationary pressures and the major Central Banks signalled a slowdown in the pace of interest rate hikes. Furthermore, public discontent in China accelerated the Government’s relaxation of Covid restrictions, further helping the global mood.

We have continued with our process of lowering volatility, which were detailed in our previous updates and fund switch notifications. We are pleased with the current positioning in the portfolios and continue to look for opportunities that develop as a result of the market conditions.

Q4 REVIEW

Market Performance

Year on year US CPI (inflation) continued to fall over the quarter, coming down to 7.1%, below consensus estimates. It was encouraging to see the core components also easing back in the recent data releases, which are more of a focus for the US Fed. Expectations for the next data point suggest a further drop in the headline rate to 6.5%. UK CPI on other hand crept back up after some relief, hovering at around 10.1%, however, expectations are for this to also come down in the near term.

Equities and bonds continued to move in tandem but this time in an upward direction, with November in particular being better for the bonds markets. The equity markets did give some of the gains back in December but managed to hold on to the majority over the quarter.

We continued to see sector dispersions, with the more cyclical sectors such as Industrials and Materials doing well. However, in keeping with the 2022 theme, the Consumer Discretionary and Technology sectors struggled due to the unfavourable environment.

From a Geographical perspective, the FTSE 100 performed well, outperforming the US markets. Following a weak start, the Asian markets rebounded as the news flow from China improved.

In other news, one of the largest crypto currency platforms, FTX, collapsed leading to billions in Dollars of losses. Whilst the saga is still unfolding, with suggestions of fraud, we suspect significantly tighter financial conditions are partly to blame. Although we do not invest in crypto linked assets, this is an example of why we are actively avoiding the more speculative and poorer quality areas of the markets as detailed later in the note.

2023 OUTLOOK

Inflation & Central Banks

The inflation picture appears to be following our expectations as detailed in our previous commentaries; we expected inflationary pressures to begin easing.

Energy and broader commodity prices have continued to fall, helping to reduce the year-on-year inflation data. Furthermore, the core components of inflation are also showing signs of easing back. The reason we expected this to occur is because of the speed and magnitude in the tightening of financial conditions; there was a high probability that inflation will ease with this backdrop. Of course, this was the intention of the Central Banks and their actions appear to be working.

This has prompted a change in tone from the Central Banks, where the US Fed has signalled a slow down in the pace of interest rate hikes. Their latest statements suggest they intend to stop raising interest rates this year and then maintain the terminal rate for a prolonged period of time to ensure inflationary pressures continue to abate. This suggests the environment will remain challenging for certain industries and businesses of poorer quality.

We expect inflationary pressures to continue easing over the coming months but to settle above the medium term historical average of 2%. We would not be surprised if inflation remained above 4% over the coming years and averaged a higher figure.

Recession Risk

Some of the key US economic data, such as housing, is suggesting we are on the cusp of a recession, if not already in one; housing data has been deteriorating sharply. The UK is following suit with house prices having fallen for four months in a row. This should not come as a surprise due to the aggressive monetary policy we have seen.

Recessions do not always spell bad news for the markets because it depends on the type of recession experienced. There is a growing consensus that the US may experience a ‘mild’ recession.

The risk here is that poorer quality businesses may suffer due to higher input costs combined with slowing demand. We have been concerned about this for some time and have worked hard to ensure the portfolios are predominantly invested in high quality businesses. These are typically companies that are profitable and have pricing power, as well as scoring well on a number of other financial metrics. We believe the markets will finally look at the fundamental merits of these types of companies again which should bode well for our portfolios.

Strategy

As mentioned at the start of the update, we have remained fully invested but have adjusted the positioning to reduce the volatility levels and better navigate the current environment. Some points to note around our thinking moving forwards and generally follow the points made in the previous update:

- Elevated volatility levels are likely to become a feature of markets over the next few years and so we will maintain a lower volatility approach.

- Due to the significant falls in the bond markets, we have been reducing our alternative exposures and steadily increasing our bond exposure. The yields on offer have not been this attractive for at least 15 years. We see value again in holding bonds.

- In terms of our equity allocations, our largest equity exposure will remain towards US markets. The US Federal Reserve has made good progress in increasing interest rates and we believe they are now at the latter stages of this process. This could bode well for aspects of the US markets.

- As previously mentioned, we now have no direct exposure to Europe due to the ongoing war in Ukraine. On a look through basis, some of our global funds have select European exposures and these are typically in the high quality international companies such as Roche and ASML.

- We are not changing the allocation to the UK however, we did decide to sell the funds most exposed to the domestic market very recently. We remain concerned with the domestic outlook and feel there are risks that may not be obvious. We therefore decided to park those holdings and move the assets into our other existing investments, which are predominantly exposed to large UK international businesses.

- We continue to hold a reasonable amount of Asian equities. With the change in China’s Covid policy coupled with fewer inflationary pressures, we are more optimistic in the near term on the region.

Positive Catalysts

Elaborating on the introduction, two of the three catalysts mentioned appear to be on the cards.

It is unfortunate to see the war has continued in Ukraine and the indications are currently for a protracted conflict. This is likely to continue having a considerable impact on markets and inflation globally, especially from the perspective of higher food and other commodity prices. It is of course very difficult to predict the outcome of the war, but a resolution would likely have a big positive impact on markets.

The US Fed have now suggested a pause is on the horizon, as inflation levels begin to ease and economic data deteriorates. This has provided some support to the markets, especially the bond markets, however we may not see a very strong recovery from this catalyst just yet. As mentioned, the US Fed intend to maintain the tighter conditions in the near term and so a policy reversal should give the markets an additional boost.

We mentioned earlier that China has eased its Covid restrictions. Whilst we had expected this at some stage, public discontent forcing the hand of the Government certainly didn’t feature as a cause for change! We believe it will be very difficult for the Government to return to their highly restrictive Covid policies and so this positive catalyst is in full swing.

Summary

Whilst the volatility in markets has continued, we are monitoring the fast-changing developments and the prospect for the inflationary pressures to continue easing.

We will continue to look for new opportunities for the portfolios whilst trying to navigate the environment the best we can.

MARKET INSIGHTS WEBINAR

If you missed our recent webinar or you would like to revisit it, please click on the recording below to watch at your convenience.

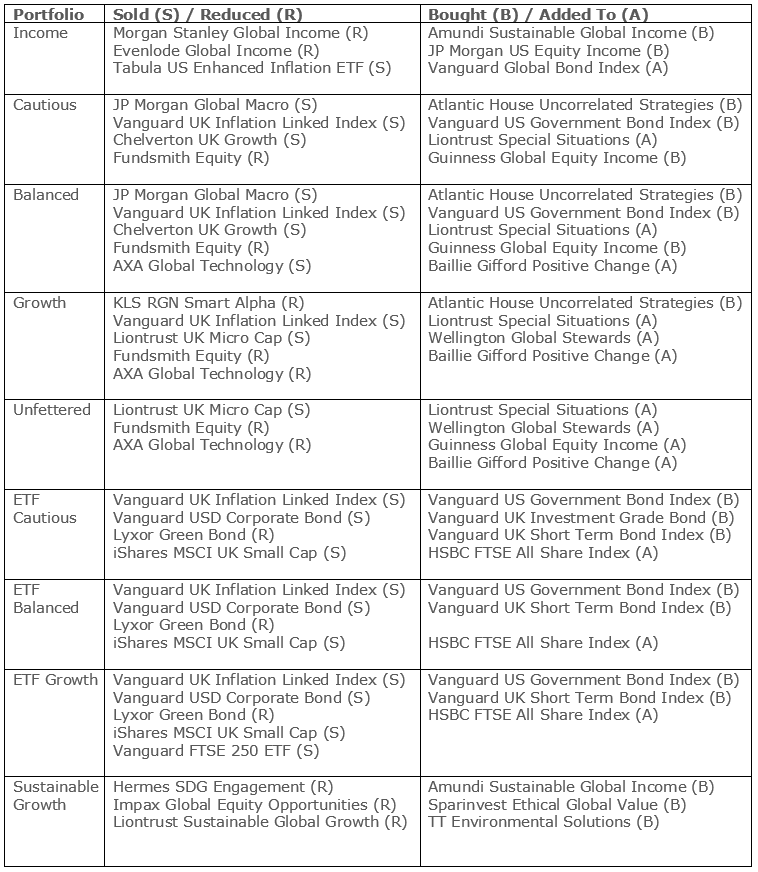

CHANGES MADE

We have made some changes during the quarter. A full account of which can be found below:

We hope you find this review informative and look forward to hearing from you if you have any questions.

This publication has been prepared for information purposes only by Carrington Investment Consultants Ltd t/a Carrington Wealth Management and does not constitute financial or investment advice. The value of investments, and any income generated from them, will be affected by interest rates, exchange rates, general market conditions and other political, social and economic developments, as well as by specific matters relating to the assets in which it invests. Investors should be aware that the value of units may well fall as well as rise, is not guaranteed and that past performance is not a guide to future performance. Different funds carry different levels of risk and investors may not get back the full amount invested.